Key Takeaways

- The Second Amendment Foundation filed a motion for summary judgment against California’s 11% excise tax on firearms, claiming it unconstitutionally discriminates against a civil right.

- SAF argues that purchasing firearms is protected by the Second Amendment, drawing parallels between this tax and First Amendment tax cases.

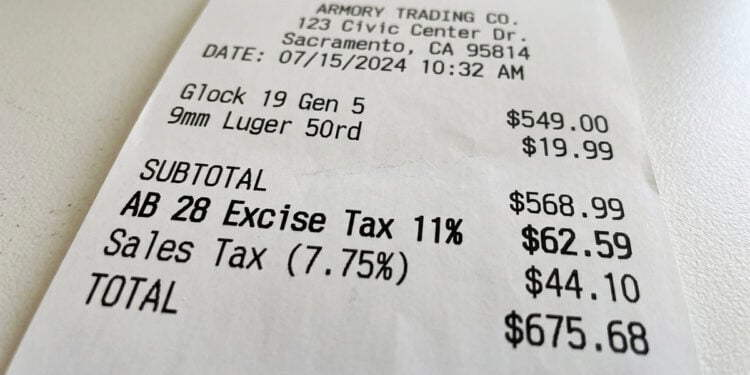

- California enacted this tax through Assembly Bill 28 in September 2023, effective July 1, 2024, with proceeds funding gun violence prevention.

- The plaintiffs, Poway Weapons & Gear and Sacramento Gun Range, have remitted significant tax payments and sought refunds, which were denied.

- If the tax stands, SAF warns it could lead to unlimited tax increases on constitutional rights.

Estimated reading time: 3 minutes

SACRAMENTO, CA — The Second Amendment Foundation filed a motion for summary judgment this week against California’s 11% excise tax on firearms and ammunition, arguing the tax unconstitutionally singles out the exercise of a fundamental civil right for disfavored treatment.

SAF filed the motion alongside plaintiffs Poway Weapons & Gear and Sacramento Gun Range on April 8 in Sacramento Superior Court. The case is represented by Michel & Associates and Cooper & Kirk. The hearing is scheduled for August 25, 2026 before Judge Christopher E. Krueger.

California enacted Assembly Bill 28 in September 2023, adding an 11% excise tax on the retail sale of all firearms, firearm precursor parts, and ammunition. The tax took effect July 1, 2024, and proceeds are deposited into the state’s Gun Violence Prevention and School Safety Fund.

Both dealers began collecting the tax on that date, passing the cost on to customers as a line item on receipts. Between the two plaintiffs, hundreds of thousands of dollars in quarterly tax payments have been remitted to the California Department of Tax and Fee Administration since the law took effect.

The dealers sought refunds, which the CDTFA denied, stating it lacked authority to issue refunds based on constitutional arguments without an appellate court ruling. After exhausting all administrative remedies, the plaintiffs filed suit in August 2025.

More from USA Carry:

SAF’s motion argues that buying firearms and ammunition is conduct covered by the Second Amendment’s plain text, and that the state cannot justify the tax under the historical analysis required by the Supreme Court’s 2022 decision in New York State Rifle & Pistol Association v. Bruen. The brief contends there is no historical tradition of singling out the exercise of a constitutional right for special taxation.

The motion draws a direct comparison to First Amendment tax cases, where the Supreme Court has repeatedly struck down taxes targeting newspapers and religious activity. SAF cites the court’s own language that the Second Amendment is not a second-class right subject to a different body of rules than other constitutional protections.

SAF also argues that accepting the state’s position would open the door to unlimited tax increases on any constitutional right. If an 11% tax on firearms is permissible, there would be nothing legally stopping California from imposing a 50% or 100% tax on the same right.

The case is Poway Weapons & Gear, Inc. v. California Department of Tax and Fee Administration, Case No. 25CV018964.

{kind=link}